{kind=link}

Table of Contents

| $52.07B | $90.06B | 11.58% |

|---|---|---|

| UAE Fintech Market 2026 | Projected Market 2031 | Fintech CAGR (2026-2031) |

The first era of UAE neobanking was about proving a concept – that a bank with no physical branches, no mountains of paperwork, and no queues could not only survive but thrive in one of the world’s most sophisticated financial landscapes. That bet has been decisively won. Now, as 2026 unfolds, the sector is in the thick of its second, far more consequential wave: Neobanking 2.0.

This is not an incremental upgrade. UAE Neobanking 2.0 is defined by a convergence of forces that would have seemed aspirational just three years ago: the imminent embedding of a Central Bank Digital Currency into everyday transactions, mandatory open finance frameworks forcing legacy banks to share data with digital challengers, and neobanks themselves graduating from scrappy disruptors to profitable, full-service financial platforms that rival established lenders on balance sheet size.

The UAE is one of the most important places in the world to watch this transformation unfold. With 100% smartphone penetration, an internet usage rate above 99%, a government that has placed financial technology at the heart of its Digital Economy Strategy, and a regulatory environment that has evolved from cautious observer to active architect of innovation, the conditions here are uniquely favorable.

In this article, we map the seven defining trends of the UAE Neobanking 2.0, ground them in the latest data and real-world developments, and explore what they mean for consumers, businesses, investors, and incumbents alike.

Trend 1: From Challenger to Champion – The Profitability Pivot in UAE Neobanking

For years, the bear case against neobanks was simple: they bleed money. High customer acquisition costs, generous interest rates used to lure depositors, and heavy technology investment created a growth-at-any-cost culture that skeptics said was unsustainable. The UAE’s digital banking sector has quietly dismantled this narrative.

Wio Bank, the Abu Dhabi-based digital platform bank launched in 2022 and backed by sovereign fund ADQ, telecom giant e&, First Abu Dhabi Bank, and Alpha Dhabi Holding, achieved profitability within its first full year of operation – a milestone that places it among the top 10 most profitable neobanks globally according to C-Innovation Market Research’s 2024 global profitability analysis.

The numbers tell a striking story. By the end of 2024, Wio had grown its balance sheet to over AED 37 billion (approximately USD 10 billion), representing nearly 3x year-on-year growth. By October 2025, customer deposits had surpassed AED 50 billion, reached in under three years since launch. Its total customer base grew 72% year-on-year, fuelled by a 93% surge in personal customers and 42% growth in business accounts.

Wio Bank: AED 50B+ in deposits, 72% YoY customer growth, 250,000+ retail customers and 120,000+ business clients as of late 2025 – with a cost-to-income ratio of just 44%.

What makes this profitability impressive is not just the topline but the efficiency underneath it. Wio reported a cost-to-income ratio of 44% and a revenue mix where approximately 45% of total revenue comes from non-interest sources – a sign of genuine product diversification rather than reliance on spread income alone.

CEO Jayesh Patel told Reuters in December 2025 that the bank now serves the largest number of SMEs of any institution in the UAE – a remarkable achievement for a bank barely three years old. Wio’s balance sheet is ‘multiple times higher’ than its pure-play digital banking peers. This profitability pivot matters beyond Wio. It is changing the conversation with investors, regulators, and traditional banks. A neobank that earns money changes the competitive calculus entirely.

Trend 2: The Regulatory Reset – CB Law 2025 and the September 2026 Deadline

No trend in Neobanking 2.0 is more foundational than the regulatory transformation underway. In October 2025, the Central Bank of the UAE enacted Federal Decree-Law No. (6) of 2025 – a landmark overhaul that consolidated the UAE’s entire financial regulatory framework by repealing both the 2018 Central Bank Law and the 2023 Insurance Decree-Law.

The new law dramatically expanded the CBUAE’s supervisory remit. Digital assets and digital finance activities – previously existing in a regulatory grey zone – are now fully integrated into the banking regulatory framework and subject to CBUAE licensing authority. Critically, the law moves beyond open banking to introduce open finance: regulated data-sharing frameworks spanning not just payment accounts but also wealth management, insurance, pensions, and credit scoring.

All entities operating in the UAE’s financial system – from legacy banks to emerging neobanks and fintech payment providers – have until 16 September 2026 to regularize their licensing status under the new framework. This ‘Regulatory Reset’ is not merely administrative. It represents a structural realignment that will determine which players can operate, at what scale, and in which segments.

The September 2026 compliance deadline under CB Law 2025 is a watershed moment. Entities that cannot meet the new licensing, governance, AML/CFT, and ICT risk standards will face penalties, revocation, or forced restructuring.

For neobanks and digital banks, the law creates both challenges and opportunities. On the challenge side, capital requirements, governance standards, and operational resilience obligations have all been elevated. On the opportunity side, the law explicitly licenses payment services using virtual assets, opening a formal pathway for regulated crypto payment products that previously operated in uncertainty.

The CBUAE’s Financial Infrastructure Transformation (FIT) Programme, spanning nine initiatives and targeting 2026 for ‘full integration,’ had already reached 85% completion as of early 2025. Milestones include the launch of the Jaywan domestic card scheme, the publication of an open finance regulation, and the approval of a stablecoin licensing framework – all essential infrastructure for UAE Neobanking 2.0 to operate on.

Trend 3: The Digital Dirham – A New Layer of Infrastructure

Perhaps no development in UAE financial infrastructure carries more long-term significance for neobanks than the Digital Dirham – the UAE’s central bank digital currency (CBDC). Under Federal Decree-Law No. (6) of 2025, the Dirham is now formally defined as existing in notes, coins, and digital form – giving the Digital Dirham the status of legal tender and the CBUAE a clear constitutional foundation for its rollout.

The UAE has been methodical in its CBDC development. Project mBridge – a multi-country blockchain platform involving the BIS Innovation Hub and the central banks of Hong Kong, China, and Thailand – has already conducted real-value transactions totalling over USD 22 million in cross-border pilots. The UAE’s first government Digital Dirham payment was executed via mBridge, involving the Ministry of Finance and the Dubai Department of Finance, and was settled in under two minutes.

While the retail launch encountered regulatory delays in late 2025 – with the CBUAE pausing testing amid considerations around privacy, cybersecurity, and systemic stability – the broader momentum has not stalled. Private-sector AED-backed stablecoins are filling the near-term gap. RAKBANK received in-principle approval to issue an AED stablecoin under the Payment Token Services Regulation. Zand Bank received approval for ‘Zand AED’ in November 2025. AE Coin has been operational since late 2024, and Mbank signed an MOU with Network International in January 2026 to integrate AE Coin acceptance across POS and e-commerce channels.

By 2026, all licensed financial institutions in the UAE are expected to support the Digital Dirham – marking one of the most advanced CBDC implementation programs globally. The programmable nature of the Digital Dirham could unlock entirely new revenue models for agile neobanks.

For neobanks, the Digital Dirham represents both a threat and an enormous opportunity. A threat, because a central bank-issued digital currency could theoretically disintermediate parts of the payment chain where digital banks currently add value. An opportunity, because neobanks’ superior app experiences, API infrastructure, and agile technology stacks make them better positioned than traditional banks to build compelling consumer-facing interfaces on top of Digital Dirham rails.

Trend 4: Banking-as-a-Service and Embedded Finance Go Mainstream

If Neobanking 1.0 was about building a better bank, Neobanking 2.0 is about becoming invisible – embedding financial services into the platforms, apps, and workflows that customers already use daily.

Wio Bank’s designation as the UAE’s first ‘platform bank’ was not a marketing exercise. The bank’s Banking-as-a-Service (BaaS) infrastructure allows non-bank businesses – from e-commerce platforms and HR software to health tech aggregators – to embed financial products directly into their user journeys. In January 2026, Wio launched what it described as the UAE’s first bank account specifically tailored for content creators: a free 12-month business account with automated invoicing, unlimited virtual cards, multi-currency balances, and a guaranteed AED/USD rate for cross-border work.

Zand Bank’s partnership with Taurus, a Swiss digital asset infrastructure provider, focuses on tokenization, smart contracts, wallets, and issuance capabilities – essentially the plumbing of embedded Web3 finance. In August 2025, Zand added Mastercard Move’s cross-border money movement solutions to its stack. In January 2026, it partnered with Yuze, providing digital business accounts, IBANs, and advanced business management tools to streamline SME onboarding.

The mandatory open finance regulation published by the CBUAE in June 2024 is a structural accelerator for embedded finance. By requiring all supervised institutions to participate in an API Hub with common infrastructure, the regulator has effectively mandated the raw material that BaaS models depend on.

Traditional banks are not standing still. Emirates NBD’s Liv., with close to half a million users, launched the Liv X app in March 2025 with integrated crypto trading, digital gold, UAE equities, and a dedicated Liv Lite app for children’s banking. ADCB has Hayyak, Dubai Islamic Bank has Rabbit, and Mashreq continues to develop its Neo franchise. The distinction between ‘neobank’ and ‘digital arm of a traditional bank’ is becoming increasingly meaningless – and that is precisely the point of an embedded finance ecosystem.

Trend 5: SME Banking – The Biggest Untapped Opportunity

If there is a single market segment that encapsulates the promise of UAE Neobanking 2.0, it is small and medium-sized enterprises. Approximately 60% of UAE SMEs remained underserved by traditional banks at the time of Wio’s launch – an extraordinary gap given that SMEs account for over 60% of the UAE’s non-oil GDP and employ the majority of the private sector workforce.

The reasons for this underservice were structural, not accidental. Traditional bank account opening for SMEs was slow, documentation-heavy, and expensive. Legacy KYC processes required physical visits, manual verification of trade licenses, and lengthy wait times. For a startup founder or a freelancer navigating mainland and freezone licensing, the friction was prohibitive.

Wio Bank cracked this problem by connecting directly to the UAE’s national identity systems and company registration data, cutting average SME account-opening times to approximately two days. The bank has since deepened this advantage through strategic integrations with health tech platforms, payment aggregators, accounting software, and trade licensing authorities across both mainland and freezone jurisdictions. Supply chain financing and credit products have been added to the platform, transforming Wio from a basic account provider into a comprehensive SME financial operating system.

Wio now hosts the largest number of SMEs of any bank in the UAE. Its SME proposition – from supply chain financing to payroll and accounting integrations – illustrates what ‘platform banking’ looks like in practice when technology meets a genuine market need.

The SME opportunity is directly linked to the UAE’s economic trajectory. The UAE economy grew an estimated 4.9% in 2025, driven by non-oil sectors including logistics, tourism, and professional services. Every new business registered – and the UAE registers thousands monthly – is a potential new customer for a digital bank that can onboard them in 48 hours rather than 48 days. Zand Bank’s January 2026 partnership with Yuze is another signal of how digital banks are evolving beyond basic accounts to offer integrated financial management for growing businesses.

Trend 6: AI, Wealth Tech, and the Hyper-Personalization Era

UAE Neobanking 2.0 is increasingly synonymous with artificial intelligence – not as a buzzword but as the operational spine of the customer experience. The next competitive frontier is not features but intelligence: the ability to analyze financial behavior, anticipate customer needs, and deliver genuinely useful interventions at exactly the right moment.

Zand Bank describes itself explicitly as an AI-powered bank. Its product architecture is built around machine learning models that process transaction data, creditworthiness signals, and behavioral patterns to offer more responsive corporate and institutional banking. Its cross-section of traditional and decentralized finance reflects a bet that sophisticated institutional clients will increasingly want a single provider to handle both conventional asset management and tokenized asset custody.

Wio Bank’s approach to AI is more consumer-facing. Its Wio Invest platform offers UAE and global stocks, ETFs, and AI-powered investment recommendations. The Saving Spaces feature uses behavioral nudges to help customers compartmentalize savings for specific goals. For the UAE, where a large proportion of the 10+ million population are expatriates managing money across multiple currencies and jurisdictions, the need for intelligent, multi-currency, goal-oriented financial tools is acute.

AI is shifting neobanking from reactive services to predictive financial management – delivering personalized savings nudges, instant credit decisions, adaptive fraud detection, and investment guidance through a single unified interface.

The wealth management ambition of Neobanking 2.0 deserves particular attention. Wio’s CEO Jayesh Patel stated in December 2025 that the bank will focus heavily in 2026 on helping wealth clients ‘manage their long-term money better’ – and plans to launch a payments company to create a fully integrated financial ecosystem. This ambition to move from transactional banking to comprehensive wealth management means UAE neobanks are now competing directly with private banks and wealth managers, not just retail lenders. The Islamic finance dimension – with growing demand for Sharia-compliant digital banking products, halal investment screeners, and ethical finance tools – adds further depth to this opportunity.

Trend 7: Cross-Border Payments and the Remittance Revolution

The UAE’s demographic makeup makes it one of the world’s most important markets for cross-border payments. With expatriates comprising over 88% of the population and remittances representing one of the country’s largest financial flows, the ability to send money internationally – quickly, cheaply, and transparently – is not a premium feature. It is table stakes.

UAE Neobanking 2.0 is addressing this with a combination of real-time payment infrastructure, stablecoin integration, and bilateral CBDC corridors. The CBUAE’s Aani real-time payment system now enables instant peer-to-peer and peer-to-merchant payments domestically, and is being linked with India’s UPI – a development of enormous significance given that India is the UAE’s largest remittance destination.

The mBridge platform, connecting the UAE, China, Hong Kong, and Thailand via a multi-CBDC infrastructure, offers a glimpse of where wholesale cross-border payments are heading: instant settlement in central bank money at a fraction of the costs of correspondent banking. Over USD 22 million in real-value transactions have already flowed through mBridge pilots, which reached minimum viable product status in June 2024.

The UAE-India UPI-Aani corridor, the mBridge multi-CBDC platform, and AED-backed stablecoins are collectively reshaping cross-border payment economics – and neobanks who integrate these rails fastest will earn outsized customer loyalty.

For neobanks, this infrastructure evolution is a double-edged sword. Cheaper rails reduce revenue from cross-border payment margins. But banks that integrate most seamlessly with new infrastructure will earn customer loyalty through superior experience. Wio’s CEO has flagged stablecoins as a key tool for cutting transaction costs. Zand Bank’s Mastercard Move integration addresses wallet-funding and cash-pick-up use cases across multiple markets. The programmable nature of cross-border payments – releasing funds conditionally based on trade milestones or invoice verification – could generate significant fee income for neobanks that build smart contract infrastructure on top of these rails.

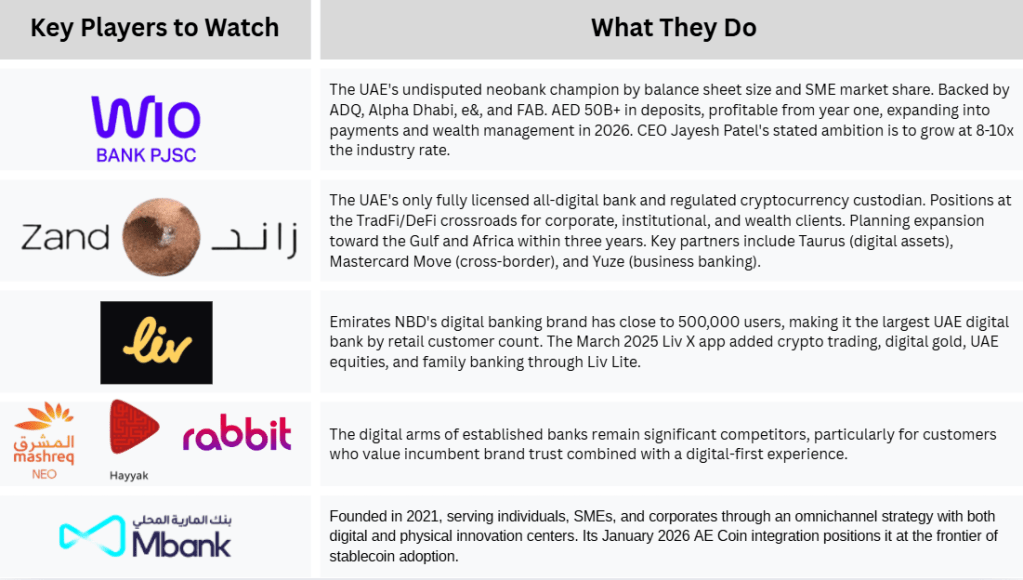

The Competitive Landscape: Key Players to Watch

Wio Bank (Abu Dhabi)

The UAE’s undisputed neobank champion by balance sheet size and SME market share. Backed by ADQ, Alpha Dhabi, e&, and FAB. AED 50B+ in deposits, profitable from year one, expanding into payments and wealth management in 2026. CEO Jayesh Patel’s stated ambition is to grow at 8-10x the industry rate.

Zand Bank (Dubai)

The UAE’s only fully licensed all-digital bank and regulated cryptocurrency custodian. Positions at the TradFi/DeFi crossroads for corporate, institutional, and wealth clients. Planning expansion toward the Gulf and Africa within three years. Key partners include Taurus (digital assets), Mastercard Move (cross-border), and Yuze (business banking).

Liv. (Dubai)

Emirates NBD’s digital banking brand has close to 500,000 users, making it the largest UAE digital bank by retail customer count. The March 2025 Liv X app added crypto trading, digital gold, UAE equities, and family banking through Liv Lite.

Al Maryah Community Bank / Mbank (Abu Dhabi)

Founded in 2021, serving individuals, SMEs, and corporates through an omnichannel strategy with both digital and physical innovation centers. Its January 2026 AE Coin integration positions it at the frontier of stablecoin adoption.

Mashreq Neo, ADCB Hayyak, and DIB Rabbit

The digital arms of established banks remain significant competitors, particularly for customers who value incumbent brand trust combined with a digital-first experience.

Challenges: What Could Slow UAE Neobanking 2.0?

- Persistent Cybersecurity Threats: The expansion of data usage and API integrations has increased the “attack surface” for digital banks, meaning a single high-profile breach could severely damage consumer trust across the industry.

- Rising Regulatory Costs: The introduction of CB Law 2025 has significantly increased the compliance burden; for smaller fintechs, the high costs of AML/CFT systems and risk controls may force market consolidation.

- Aggressive Incumbent Competition: Major traditional banks (such as Emirates NBD, FAB, ADCB, and Mashreq) are closing the digital gap by combining their massive liquidity and brand trust with increasingly sophisticated digital interfaces.

- Erosion of the Digital-Only Moat: The simple advantage of “being digital” is disappearing as legacy banks transform, making it harder for pure-play neobanks to compete on technology alone.

- Complexity of Cross-Border Expansion: Expanding across the GCC is a slow, multi-year process due to the challenges of navigating diverse regulatory requirements, local partnership requirements, and cultural adaptations.

What’s Next: The UAE Neobanking 2026 Roadmap

As 2026 progresses, several developments will define whether Neobanking 2.0 achieves its full potential. The September 2026 regulatory compliance deadline under CB Law 2025 will be a defining moment – entities that meet the new standards will emerge stronger; those that do not may face restructuring, acquisition, or exit. Watch for consolidation among smaller players.

The Digital Dirham’s commercial trajectory remains the single most-watched variable. If the CBUAE can resolve privacy and cybersecurity concerns and move toward public availability, it will fundamentally reshape the payment landscape. Neobanks ready to integrate will gain significant first-mover advantages.

Open finance, mandated by the CBUAE’s June 2024 regulation and backed by CB Law 2025, will begin delivering its first real consumer benefits as the API Hub infrastructure matures. Expect new products combining banking, insurance, wealth, and pension data in ways that were previously impossible. Wio’s 2026 payments company launch and Zand Bank’s Gulf and Africa expansion ambitions are both milestones worth tracking closely.

Conclusion

UAE Neobanking 2.0 is not just a local story. It is a global proof of concept for what digital banking looks like when government ambition, regulatory sophistication, tech-first infrastructure, and a high-income, digitally native population converge.

The UAE fintech market is on a trajectory to nearly double to $90 billion by 2031. Wio Bank has shown that a neobank can reach profitability inside its first year, build a balance sheet of over AED 50 billion in under three years, and serve as the preferred bank for the country’s entire SME ecosystem – without a single physical branch. The Digital Dirham is pioneering programmable sovereign money. Open finance is democratizing data. Stablecoins are transforming cross-border payments. AI is personalizing financial management at scale.

For fintech founders, investors, regulators, and traditional banks watching from the outside, the message from the UAE in 2026 is clear: the second generation of digital banking has moved beyond disruption into dominance. The question is no longer whether neobanks will reshape finance – but which ones will lead it, and how fast.

The UAE is not experimenting with the future of banking. It is building it – and Neobanking 2.0 is the clearest signal yet that the future has arrived ahead of schedule.